🎙️ FX Talk | Get updated on what's happening on the financial markets in 20 min. listen here.

-

AU

-

Australia - English

- België - Nederlands

- Belgique - Français

- Canada - English

- Canada - Français

- Česká Republika - Čeština

- Deutschland - Deutsch

- España - Español

- France - Français

- Ελλάδα - Ελληνικά

- Hong Kong - English

- Italia - Italiano

- Luxembourg - English

- Nederland - Nederlands

- Polska - Polski

- Portugal - Português

- România - Română

- Schweiz - Deutsch

- Suisse - Français

- United Arab Emirates - English

- United Kingdom - English

- Hong Kong-Traditional Chinese

-

Australia - English

Ebury London

100 Victoria Street

London

SW1E 5JL

+44 (0) 20 3872 6670

[email protected]

Ebury.com

Sterling edges lower as UK inflation comes in unrevised for July

- Go back to blog home

- Latest

15 August 2017

Senior Market Analyst at Ebury. Providing expert currency analysis so small and mid-sized businesses can effectively navigate international markets.

The major currencies traded within a relatively narrow band on Monday with a lack of any news during typically quiet August trading leading to a quiet session of foreign exchange trading.

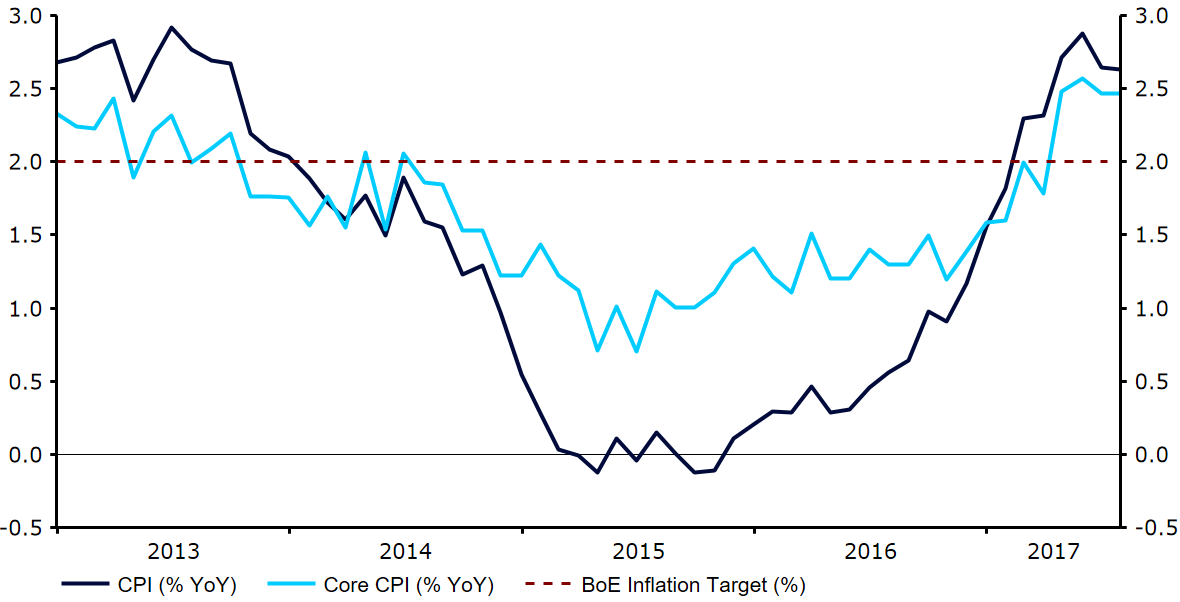

This morning’s inflation numbers led to a modest sell-off, remaining unrevised in July at 2.6% versus the 2.7% consensus (Figure 1). We continue to think that as inflation edges back towards the 3% level investors will begin to bring forward expectations for an interest rate hike by the Bank of England.

Figure 1: UK Inflation Rate (2013 – 2017)

The US Dollar was broadly stronger across the board yesterday as a return in risk appetite following last week’s developments out of North Korea led to a sell-off in the traditionally “safer” currencies. Today’s US retail sales, seen by the Federal Reserve as one of the main economic data releases of the month, could shift the currency this afternoon. Ahead of Thursday’s FOMC meeting minutes, financial markets have continued to push their expectations for the next interest rate increase by the Fed and are now pricing in the next hike as far out as June 2018.

In the Eurozone, industrial production was a slight disappointment in June with output declining 0.6% from the downwardly revised 1.2% registered in May. Thursday’s inflation numbers and European Central Bank meeting accounts are undoubtedly the main focal points of the week in Europe. In the run-up to these announcements the Euro is likely to remain fairly range bound, barring any significant new rhetoric from either Donald Trump or North Korean authorities that could provide a catalyst for a renewed shift to safe havens., Hi, I am a new blog post, you can change me, or even delete me!, it is up to you! 😉

SHARE

Cookies and Privacy

This site uses cookies to ensure you get the best experience. For more information see our Privacy NoticeAccept Settings Reject

Privacy Overview

| Cookie | Duration | Description |

|---|---|---|

| cookielawinfo-checkbox-advertisement | 1 year | The cookie is set by GDPR cookie consent to record the user consent for the cookies in the category "Advertisement". |

| cookielawinfo-checkbox-analytics | 11 months | This cookie is set by GDPR Cookie Consent plugin. The cookie is used to store the user consent for the cookies in the category "Analytics". |

| cookielawinfo-checkbox-functional | 11 months | The cookie is set by GDPR cookie consent to record the user consent for the cookies in the category "Functional". |

| cookielawinfo-checkbox-necessary | 11 months | This cookie is set by GDPR Cookie Consent plugin. The cookies is used to store the user consent for the cookies in the category "Necessary". |

| cookielawinfo-checkbox-others | 11 months | This cookie is set by GDPR Cookie Consent plugin. The cookie is used to store the user consent for the cookies in the category "Other. |

| cookielawinfo-checkbox-performance | 11 months | This cookie is set by GDPR Cookie Consent plugin. The cookie is used to store the user consent for the cookies in the category "Performance". |

| viewed_cookie_policy | 11 months | The cookie is set by the GDPR Cookie Consent plugin and is used to store whether or not user has consented to the use of cookies. It does not store any personal data. |

| Cookie | Duration | Description |

|---|---|---|

| _ga | 2 years | This cookie is installed by Google Analytics. The cookie is used to calculate visitor, session, campaign data and keep track of site usage for the site's analytics report. The cookies store information anonymously and assign a randomly generated number to identify unique visitors. |

| _ga_DGRPXRE06R | 2 years | This cookie is installed by Google Analytics. |

| _gat_gtag_UA_51187572_49 | 1 minute | This cookie is set by Google and is used to distinguish users. |

| _gid | 1 day | This cookie is installed by Google Analytics. The cookie is used to store information of how visitors use a website and helps in creating an analytics report of how the website is doing. The data collected including the number visitors, the source where they have come from, and the pages visted in an anonymous form. |

| CONSENT | 16 years 4 months | These cookies are set via embedded youtube-videos. They register anonymous statistical data on for example how many times the video is displayed and what settings are used for playback.No sensitive data is collected unless you log in to your google account, in that case your choices are linked with your account, for example if you click “like” on a video. |

| pardot | past | The cookie is set when the visitor is logged in as a Pardot user. |

| Cookie | Duration | Description |

|---|---|---|

| IDE | 1 year 24 days | Used by Google DoubleClick and stores information about how the user uses the website and any other advertisement before visiting the website. This is used to present users with ads that are relevant to them according to the user profile. |

| test_cookie | 15 minutes | This cookie is set by doubleclick.net. The purpose of the cookie is to determine if the user's browser supports cookies. |

| VISITOR_INFO1_LIVE | 5 months 27 days | This cookie is set by Youtube. Used to track the information of the embedded YouTube videos on a website. |

| YSC | session | This cookies is set by Youtube and is used to track the views of embedded videos. |

| yt-remote-connected-devices | never | These cookies are set via embedded youtube-videos. |

| yt-remote-device-id | never | These cookies are set via embedded youtube-videos. |

| Cookie | Duration | Description |

|---|---|---|

| _lfa | 2 years | This cookie is set by the provider Leadfeeder. This cookie is used for identifying the IP address of devices visiting the website. The cookie collects information such as IP addresses, time spent on website and page requests for the visits.This collected information is used for retargeting of multiple users routing from the same IP address. |