Pound strengthens after impressive UK GDP growth figures

- Go back to blog home

- Latest

27 October 2016

Senior Market Analyst at Ebury. Providing expert currency analysis so small and mid-sized businesses can effectively navigate international markets.

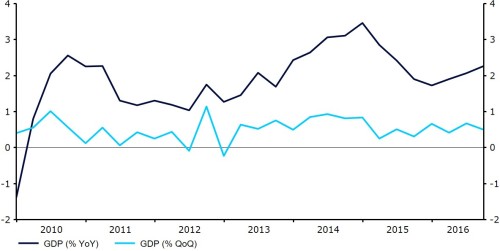

Sterling spiked against its major peers this morning after a surprisingly resilient set of GDP numbers alleviated concerns that the UK economy could be set for a sharp slowdown in the second half of the year following June’s Brexit vote.

Figure 1: UK GDP Growth Rate (2010 – 2016)

The Pound had earlier edged higher on Wednesday, rebounding back above the 1.22 level against the US Dollar following Tuesday afternoon’s comments from Governor of the Bank of England Mark Carney. Carney’s comments on the strength of the Pound, combined with this morning’s impressive GDP numbers, have alleviated concerns that the BoE could be ready to cut interest rates again before the end of the year. The majority of investors and analysts now expect the central bank to hold off, for now.

Meanwhile, the US Dollar eased from its near nine month highs, falling to a six day low against the Euro on uncertainty surrounding both the Federal Reserve’s interest rate decision next week and the pending Presidential Election. Implied probability of a hike at December’s FOMC meeting slipped to around 74% from closer to 80% yesterday, despite mostly positive economic news that saw the US services PMI rise more than expected to an eleven month high of 54.8 from 52.3.

The Euro almost completely overlooked a report from Reuters that revealed European Central Bank sources had claimed the ECB is all but certain to extend its quantitative easing programme beyond the existing March 2017 timeframe.

Impressive inflation data in Australia also eased concerns that the Reserve Bank of Australia could be ready to slash interest rates again. Headline consumer price growth in the third quarter rose sharply to 1.3% from the 1.1% consensus, possibly pushing back the next RBA interest rate cut until next year.

Major currencies in detail:

GBP

The Pound rebounded from Tuesday’s near three week low against the US Dollar yesterday, appreciating 0.5%.

No news was good news for Sterling yesterday, with a lack of any significant political developments providing some relief for the UK currency. Traders instead awaited this morning’s GDP numbers, while looking ahead to next Thursday’s Bank of England meeting, where policymakers could shed more light on the likelihood of another interest rate cut in the UK.

Mortgage approvals were the only data release of note. Approvals fell to a 19 month low 38,252, down 15% on a year previous.

Third quarter GDP numbers this morning will be the main economic release ahead of next week’s Bank of England meeting.

EUR

Despite little economic news out of the Euro-area on Wednesday, the single currency rebounded 0.2%.

Consumer confidence in Germany dipped slightly this month according to the monthly survey from GfK. The index fell to 9.7 from 10 last month, although did little to shift the Euro which was driven largely by technical factors.

Elsewhere, a survey published by think-tank Demos suggested that Euroscepticism was on the rise across Europe. 40% of those surveyed were pessimistic about the European Union over the next twelve months compared with just 12% that are optimistic.

With no major economic releases in the Eurozone today, the Euro will likely be driven by events elsewhere. German inflation data on Friday will be next up for the Euro.

USD

Lingering uncertainty over the timing of the Federal Reserve’s next interest rate hike sent the US Dollar 0.1% lower against its major peers on Wednesday.

New home sales in the US increased in September, rising to 593,000 from August’s 575,000. While this was below forecast, the average pace of sales in the third quarter remained at a very solid 599,000, marking its highest level since the final quarter of 2007 and suggesting that underlying conditions in the US housing market remains healthy.

In another positive development, the goods trade deficit also fell in September by $2 billion to $56 billion. Yesterday’s robust numbers bode well for Friday’s GDP numbers, which could be on course to exceed the 2.7% estimate.

Durable goods orders data this afternoon will be the main economic release at 13:30 UK time this afternoon. Orders are expected to print almost flat in September for the second straight month.

Receive these market updates via email

SHARE