Euro approaches five week low after hawkish Fed speeches

- Go back to blog home

- Latest

22 February 2017

Senior Market Analyst at Ebury. Providing expert currency analysis so small and mid-sized businesses can effectively navigate international markets.

The Euro slumped to just shy of its weakest position against the US Dollar in five weeks on Tuesday after another relatively hawkish speech from a Federal Reserve policymaker kept the door firmly open to an interest rate hike by the central bank at its next meeting in March.

Euro traders almost completely overlooked yesterday’s strong business activity PMI’s, suggesting that investors remain wary of downside risks from political developments in the Eurozone, namely the important elections in the Netherlands and France.

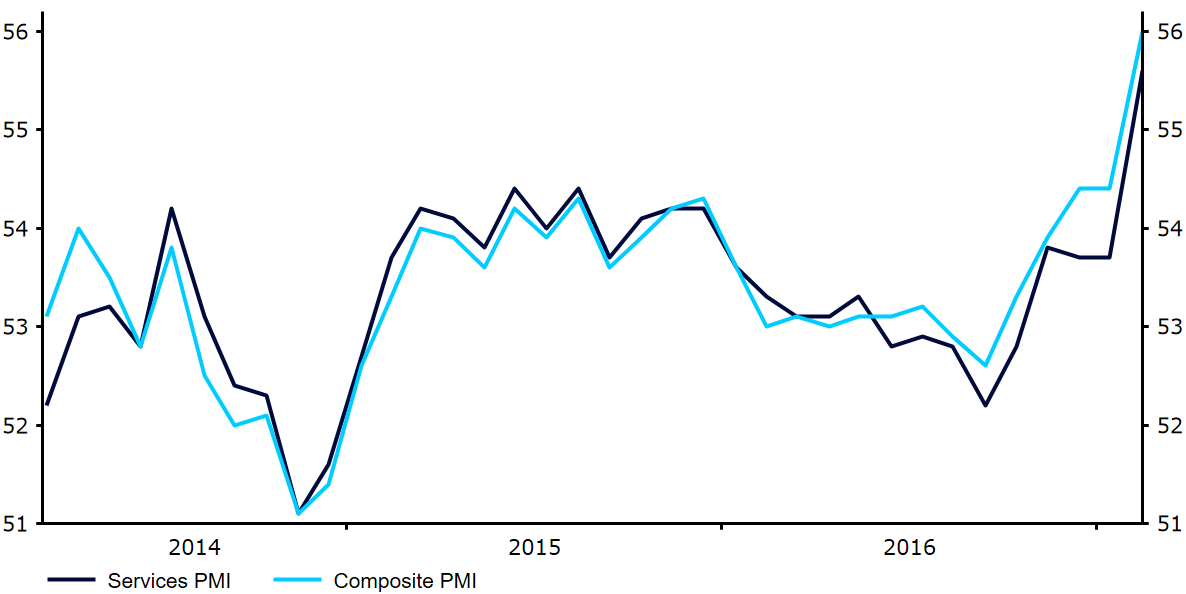

Tuesday’s PMI’s, a key gauge of growth in the economy, all came in comfortably above expectations. The composite index, of which measures a weighted combination of activity in both the manufacturing and services sectors, rose to 56.0 from 54.4, its highest reading since April 2011 (Figure 1). This reinforces our view that the Eurozone economy is recovering faster than originally expected which should lessen the need for further easing measures from the European Central Bank in the coming months.

Figure 1: Eurozone Composite PMI (2014 – 2017)

Attention today turns firmly to the Federal Reserve, which releases the minutes from its February meeting at 19:00 UK time. We expect the minutes to mostly reiterate the key messages from the statement, while keeping options open for a hike in March.

Major currencies in detail

GBP

Sterling recovered from a brief sell-off yesterday morning to end the session 0.2% higher against the US Dollar.

Governor of the Bank of England Mark Carney and a number of his fellow MPC members made a fairly low key appearance in Parliament as part of the Central Bank’s Inflation Report hearings. The BoE claimed that it has made “big improvements” in its ability to forecast the UK economy, although warned that it had little confidence in even its own predictions. Investors were left slightly disappointed by the lack of any forward guidance on the Bank’s next monetary policy move.

Bank of England member Jon Cunliffe will be speaking at 11:00 UK time. An updated set of fourth quarter GDP numbers are expected to remain unrevised this morning and show the UK economy grew 0.6% in the final four months of last year.

EUR

The Euro fell 0.3% during London trading on Tuesday as events elsewhere and concerns over upcoming European elections completely overshadowed the solid economic news released in the Euro-area.

Yesterday’s PMI‘s for February were broadly impressive. Manufacturing activity expanded at its fastest pace in nearly six years, with the PMI increasing to 55.5 from 55.2. The area’s dominant services sector also grew at a very healthy pace. The services PMI for the wider Eurozone area increased to 55.6 from 53.7, also its highest reading since 2011. This was fuelled largely by a greater-than-expected expansion in Germany and France.

Revised inflation figures for the Eurozone this morning are expected to remain unchanged. Political risks continue to be the main driver in Europe and we could see the common currency test its recent five week low today.

USD

The US Dollar index rose 0.25% on Tuesday amid ramped up expectations for a hike at the Fed’s March meeting.

The Dollar did, however, retrace some of its gains yesterday afternoon after the latest manufacturing and services PMI’s showed that business activity in the US may have begun to slow so far this year. The manufacturing PMI slumped to 54.3 from 55.0, its lowest level in three months. The services sector also suffered from a fairly abrupt slowdown, with the index declining 1.7 points to 53.9.

The release of the Federal Reserve’s meeting minutes this evening will be the main economic announcement in the currency markets today.

SHARE